Purdue University Muni Deal Threatens Over 20% Loss for Holders ...

(Bloomberg) -- Fans of the Purdue University Boilermakers are reveling in victory after the top-ranked college basketball team trounced Grambling State and Utah State in the NCAA’s March Madness Tournament over the weekend.

It’s a different story in the debt market, where investors in the college’s bonds are poised to take a loss as Purdue prepares to exercise an obscure provision to call back securities before they are due.

The university — equipped with a $2.7 billion endowment and a AAA credit rating — is replacing Build America Bonds it sold more than a decade ago with lower yielding tax-exempt debt as part of a $72 million bond sale this week. Purdue is looking to buy back those bonds at close to par, or 100 cents on the dollar. But the debt has recently traded above that level.

Take the investor who in December 2021 bought debt sold by the top-rated university at 130.4 cents on the dollar. That buyer could theoretically take a more than 20% loss on an otherwise safe investment. Even more recent investors will take a hit – debt due in 2035 last traded at 105.5 cents on the dollar.

Nicole Michienzi, senior director for capital markets at Purdue, declined to comment.

The situation with Purdue is just one example of several in the muni market that has investors, well, boiling.

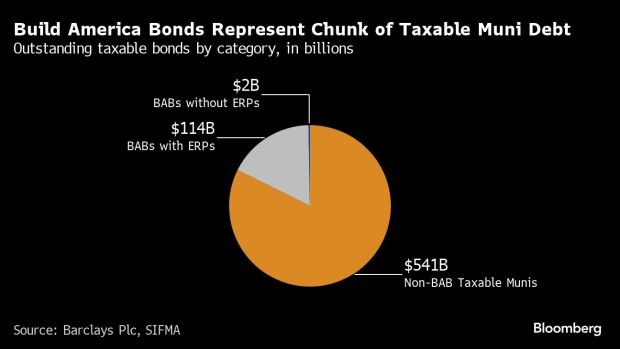

The controversy stems over municipalities and schools’ effort to cut their borrowing costs on bonds they sold as part of an Obama-era program meant to kickstart the economy through infrastructure spending after the Great Recession. The federal government was supposed to subsidize 35% of the interest costs on the so-called Build America Bonds, only to cut the subsidy in 2013 during sequestration.

Years later, muni issuers that sold Build America Bonds are refinancing them by taking advantage of provisions included in the deals. For example, offering documents for Purdue’s 2010 transaction say the college could execute a call of the bonds if an “extraordinary event” occurs. Such an event would be a “material adverse change” to the tax code where the US Treasury reduces that 35% subsidy, the documents state.

‘Extraordinary’ Event

The refinancings started emerging after a recent court decision ruling lent credence to the argument that the subsidy cuts qualified as an extraordinary event. Orrick, a major law firm to municipalities, said the US Court of Federal Claims’s decision involving an Indiana power agency’s bonds supports the conclusion that sequestration resulted in a materially adverse change.

“A recently concluded court case provides favorable guidance for issuers,” attorneys at Orrick said in a February report. “Although the specific language must be reviewed in each case, we believe extraordinary optional redemption is available for issuers of BABs in most cases.”

An extraordinary redemption provision was included in nearly all the $100 billion of the Build America Bonds still outstanding.

Meanwhile, the recent strength of the muni market makes selling tax-exempt securities look extra appealing. Yields have plunged compared to their taxable debt. Since February, a number of municipalities have started refinancing the bonds with new tax-exempt debt, as Purdue is doing.

Other governments have much more BAB debt outstanding, making the stakes even greater for investors. The University of California is facing pushback from investors on a $1 billion bond sale earlier this month. Bondholders hired a law firm to dispute the deal.

Purdue’s Build America Bonds were sold for campus projects like a student fitness and wellness center. About $60 million of principal is outstanding and being called as part of the extraordinary redemption, according to a filing by the school on March 20.

©2024 Bloomberg L.P.