Google: AI Boost Heading Into Q2

hapabapa

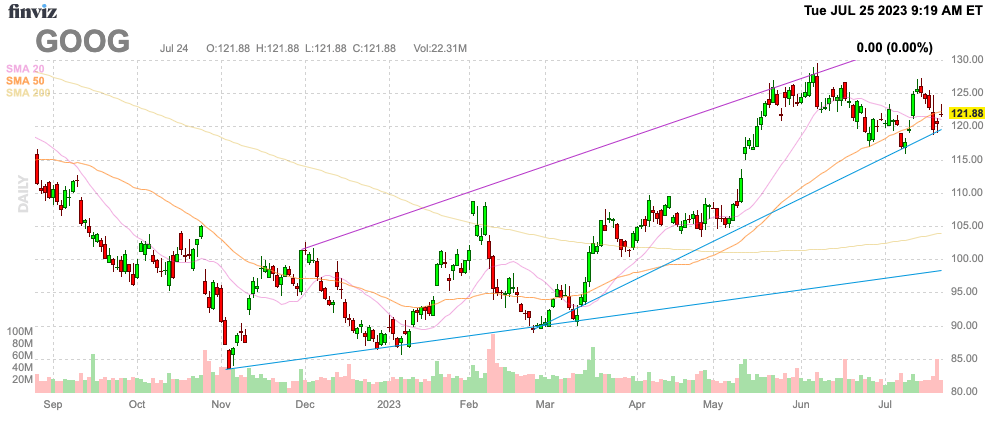

One major outcome of the apparent Apple Inc. (AAPL) AI endeavor is a heavy reliance on Alphabet Inc. (NASDAQ:GOOG, NASDAQ:GOOGL), aka Google. The tech giant has invested heavily in AI tools over the last several years and appears well-positioned with Google Cloud to benefit from surging demand for data center space. My investment thesis remains ultra Bullish on Google heading into Q2 '23 earnings after the close on Tuesday, July 25.

Finviz

Google CloudThe interesting revelation about the Apple AI plans was the use of both Google Jax and Google Cloud. The long battle between Apple and Microsoft Corporation (MSFT) might naturally preclude Apple from working with Microsoft, leaving Google as the best choice to use their AI tools incorporated with cloud services.

While still too early to tell whether Apple makes much out of the AI plans, the market for AI could be enormous. Microsoft just launched a generative AI service called Copilot for $30/month, while Deepwater Asset Management has outlined a path to a $1+ trillion personal AI market.

Some analysts forecast an AI "tidal wave" leading to $20 billion in additional revenues for Microsoft in 2024 alone. The company is a $200+ billion sales machine, so an amount as big as $20 billion moves the needle by 10% immediately.

The interesting catch on the Microsoft AI plans is the high costs of generative AI computing power. Jefferies analyst Brent Thill sees costs jumping from $32 billion currently to $35 billion in FY24, and possibly up to $40 billion.

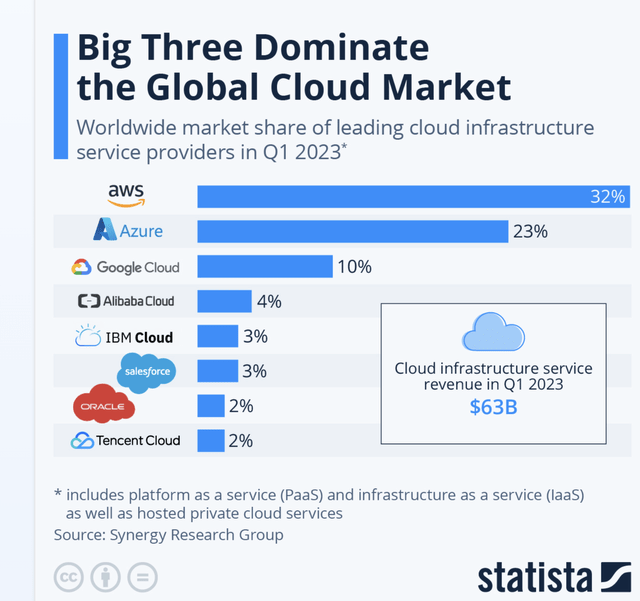

Google would very much benefit from Apple spending aggressively on generative AI by utilizing Google Cloud and other services. The company is currently the #3 global cloud provider with a 10% market share. Google is a leader in AI tools, and Apple as a customer could provide a major boost to the business.

Statista

Dan Ives from Wedbush forecast Microsoft could see $35 to $40 of incremental AI spend for every $100 spent on cloud. Right now, the focus is on Microsoft with Azure, but investors shouldn't look past Google Cloud, especially with Apple as a customer.

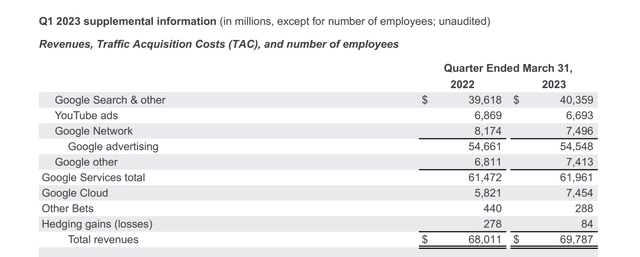

Cloud revenue was already one of the strong points for Google in Q1'23. The company saw cloud revenues surge 28% to $7.5 billion, up from only $5.8 billion in the prior year.

Google Q1'23 Earnings Release

In fact, the nearly $1.7 billion sales boost accounted for the vast majority of growth at the company in the March quarter. The numbers actually support Google having more than a 10% market share of the cloud infrastructures services market listed at $63 billion in the quarter by Statista.

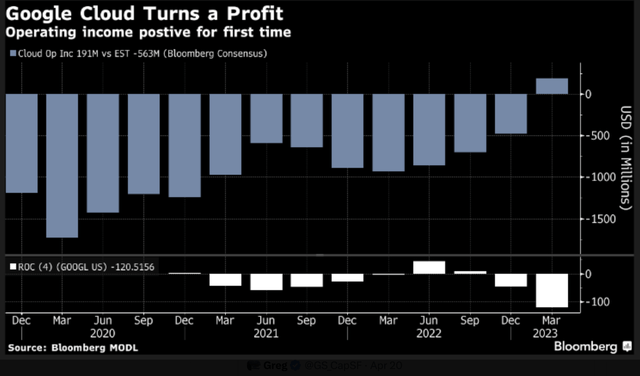

The more interesting aspect of the Google Cloud business is the sudden shift to being profitable. The business was a previous drag on Google profits, with a Q1 '22 operating loss at $706 million.

Bloomberg

A big part of the change was Google adjusting the deprecation charges for data center servers. The switch lengthens the usage period and boosted operating income by $988 million and net income by $770 million.

Last Q2, Google Cloud produced revenues of $6.3 billion. In order to maintain the same growth rate, Google needs to generate $8.0 billion in Cloud revenues in the June quarter.

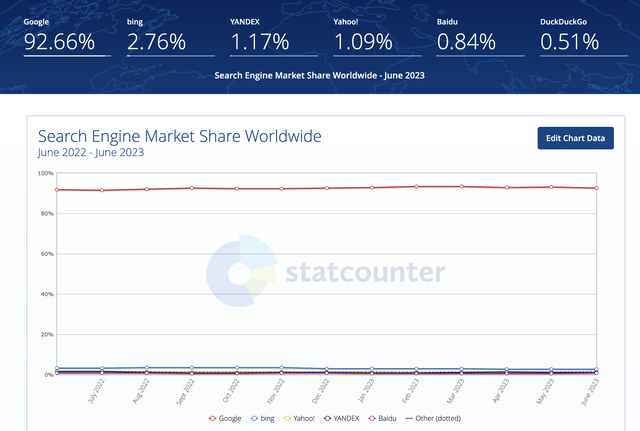

The big AI boost and the addition of Apple as an AI customer should provide some indication of future gains. Not to mention, the Search business doesn't appear one bit impacted by ChatGPT or Bing Ai, with Google still maintaining x% market share, similar to prior-year levels.

StatCounter

Analysts are forecasting total revenues to grow 4.4% in the quarter, after only 2.6% in Q1 and hardly growing in Q4 '22. Google could likely top this growth target due to AI and signal the company is back in growth mode.

Our research has already shown how Google gets to a $10 EPS target in the next few years after accounting for stock-based compensation and hitting the 20% efficiency targets set by the CEO. Investors will definitely want to watch operating expenses and employee counts to see how the tech giant has progressed on this front, and whether the generative AI push is pressuring costs while not boosting revenues.

TakeawayThe key investor takeaway is that Google should be back in growth mode, boosted by AI and Google Cloud. The tech giant has a path to a $10 EPS by 2025 and currently trades at ~14x consensus non-GAAP EPS targets when adding back ~$1.30 in stock-based compensation charges.

Google remains a cheap stock here heading into the 2H of 2023, and any bullish indications on AI chat features should boost the stock further.

If you'd like to learn more about how to best position yourself in under valued stocks mispriced by the market, consider joining Out Fox The Street.

The service offers a model portfolio, daily updates, trade alerts and real-time chat. Sign up now for a risk-free 2-week trial.